Mortgage data enables lenders to benchmark their performance and that of their business partners and competitors, making it a powerful tool for operating more profitably and with greater agility. However, not all mortgage market data is created equal.

For benchmarking data to provide valuable insights into your competitive positions, risk mitigation strategies, and market trends, it must be current, granular, and comprehensive.

Lenders who harness the power of direct-source, real-time mortgage lock data – data collected directly from lenders' ratesheets and systems – benefit from gaining current insight into market trends. It’s critical to have key variables such as rates, price, margins, concessions, LLPAs, servicing values, and production mix.

Here are four ways that leveraging mortgage data intelligence can help improve your margins and performance.

1. Optimizing Margins and Pricing Elasticity

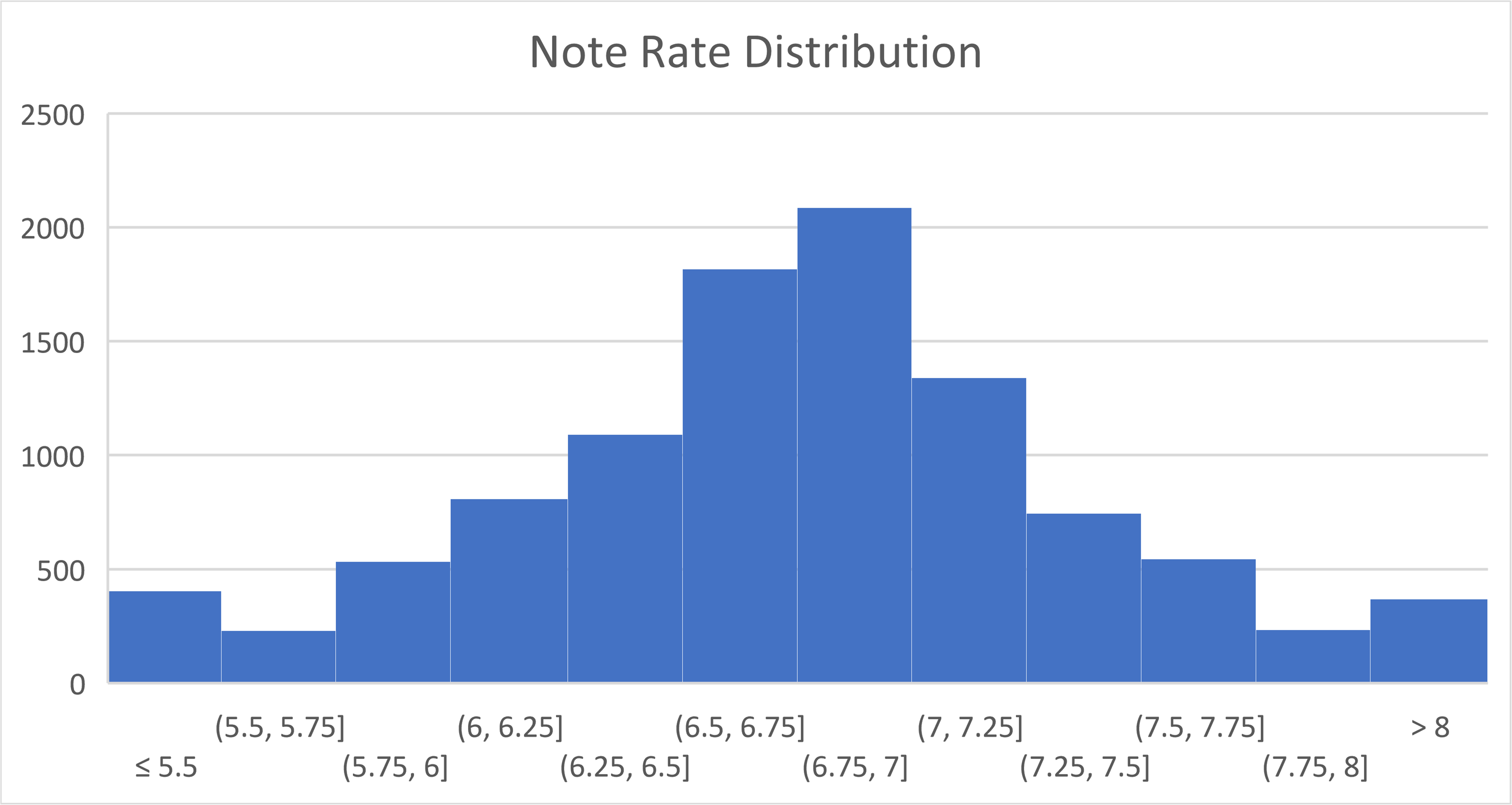

Understanding price elasticity and positioning within market trends is essential for maximizing profit margins. With data that reveals rate trends as they unfold, you can anticipate changes in the competitive landscape and adjust your strategies proactively rather than reactively.

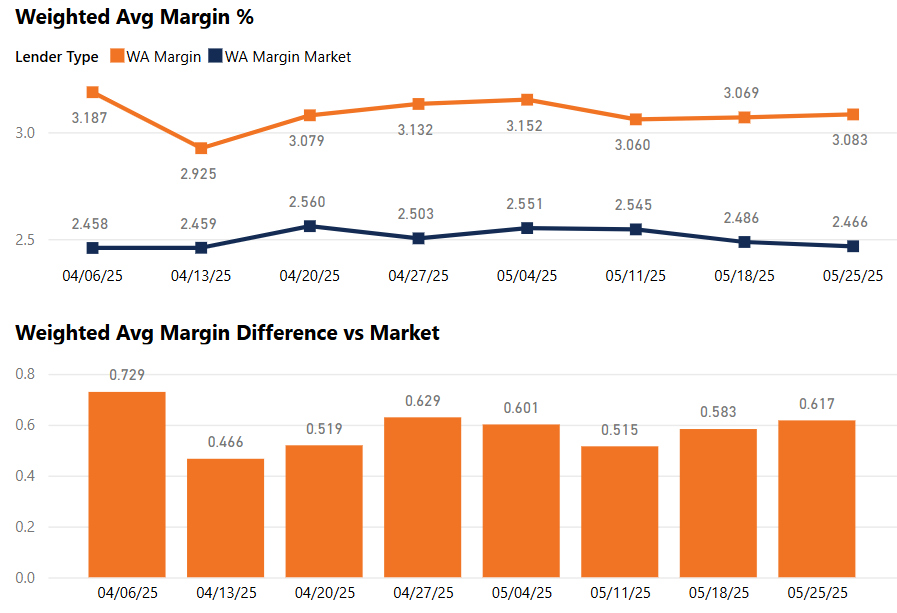

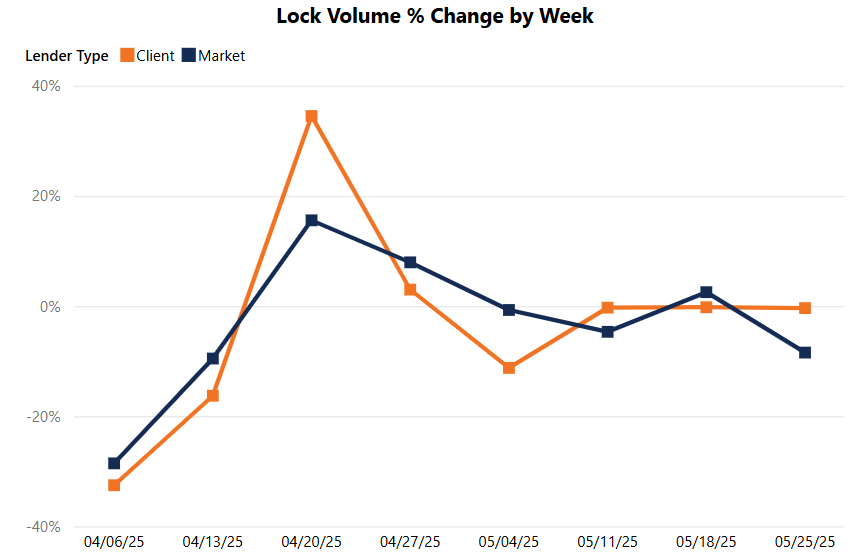

Loan level offerings allow you to fine-tune pricing to optimize the margin/volume tradeoff and reported margin data gives insight into how you compare to your peers. For instance, benchmarking daily volumes against the market and filtering the lock data for the specific target geographies and products provides you with an apples-to-apples comparison. This direct comparison allows you determine whether changes you are seeing are a result of market share gains or simply upward movement in the market overall.

Further, you can create distribution analyses with the loan level rate lock data to identify where the pockets of production are that you can target with your pricing strategy. For example, if you identify that your rate offerings are slightly above the market average, you can adjust them closer to the market’s bell curve peak to potentially increase market share while still maintaining a favorable margin.

By understanding price elasticity for your product offerings, you can identify pockets of production to target with your pricing strategy, fine-tuning your approach to optimize the margin/volume tradeoff. Such direct and immediate insights are invaluable in the secondary market, where timing and accuracy in understanding rate trends can significantly impact profitability.

2. Increasing Leads and Converting Leads to Locks

Analytics on homebuyer profiles and behavior give visibility into new opportunities, allowing you to target outreach efforts to channels and locations with the greatest return potential.

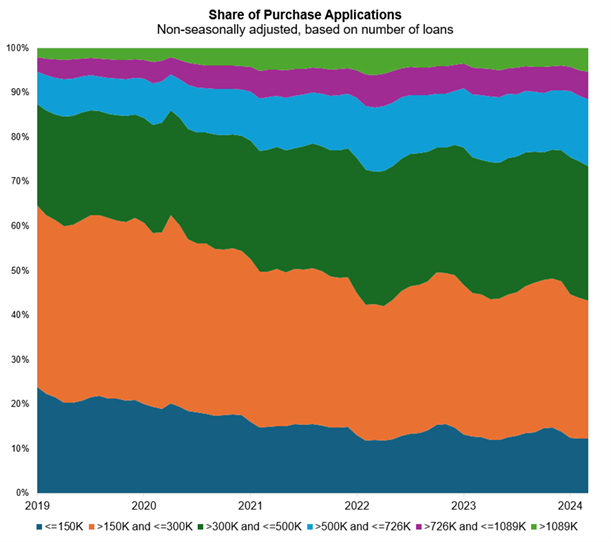

You can utilize real-time data on production characteristics – such as property types, loan amounts, borrower credit scores, and occupancy – to understand market nuances and refine marketing and sales messages accordingly.

Having visibility into competitive rate offerings enables originators to quote rates confidently. This data provides assurance that their rates are competitive, even when including discount points or other pricing strategies. Understanding the broader market helps originators position their quotes to attract rate-sensitive borrowers who are comparing multiple lenders. This strategic use of data enhances the chances of converting inquiries into locked loans, driving up the lender’s success rate.

The ability to segment data by borrower demographics or loan characteristics also helps refine lead-targeting efforts. Marketing teams can create more personalized messaging that resonates with specific borrower needs, such as first-time homebuyers or those seeking jumbo loans. This level of precision in outreach and follow-up strategies can significantly improve conversion rates.

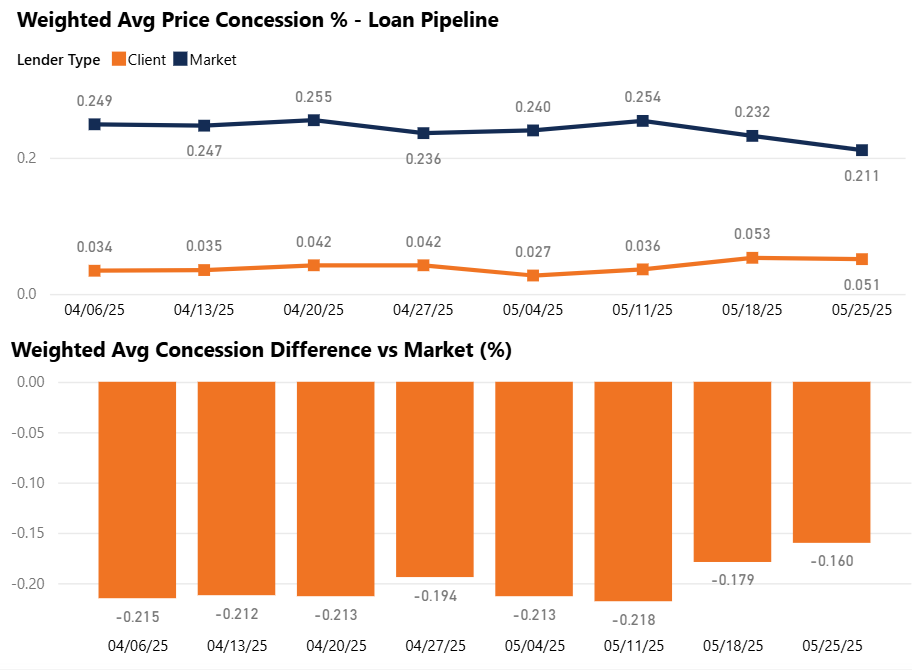

3. Reducing Concessions

Concessions are often given during rate negotiations to secure a borrower’s commitment, but excessive concessions can erode profitability. Real-time data equips originators with the competitive insights needed to minimize unnecessary concessions. By accessing detailed market data, originators can validate their rate offerings and negotiate confidently with borrowers while maintaining profitability.

For instance, if a borrower suggests they can secure a better rate elsewhere, having current market rate data allows originators to counter and hold firm on pricing unless points are paid. This data-driven confidence can lead to more favorable negotiation outcomes and reduce the frequency of concessions.

Lenders can also track concession trends over time and compare their performance to market benchmarks. This visibility enables leadership to identify if specific branches or originators are granting more concessions than necessary. With this insight, management can implement targeted training or adjust compensation models to incentivize performance that aligns with company profitability goals.

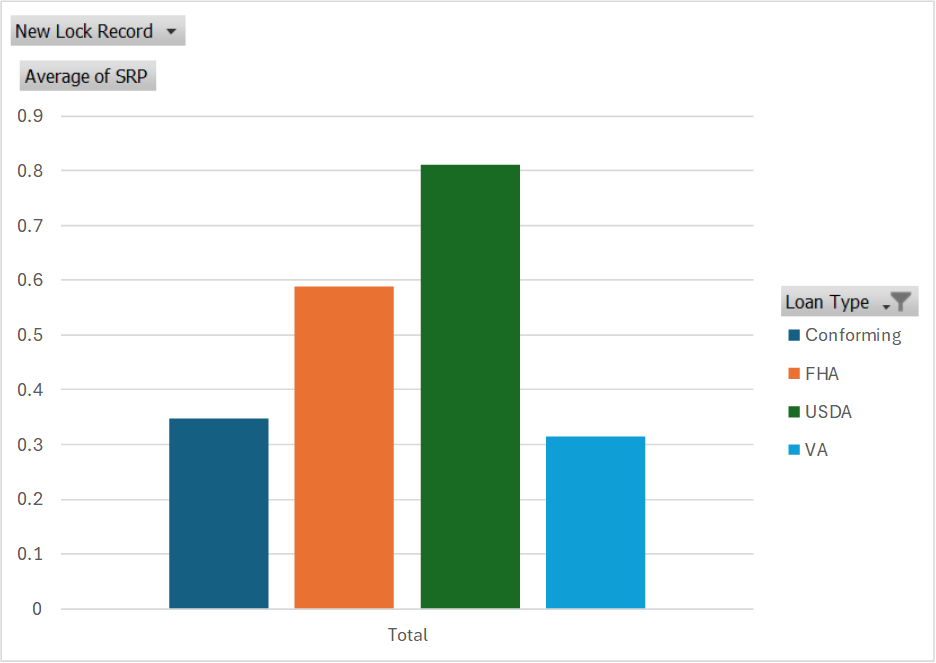

4. Improving Execution and Tracking Servicing with a Benchmark Pricing Strategy

By leveraging granular lock data, lenders can break down components of their pricing structure – including markups, LLPAs, and servicing-released premiums (SRPs) – and keep them aligned with market trends. For example, if a lender notices that their Day 1 margin is lower than the market average, they might explore adjustments to increase profitability without compromising their competitive position.

Benchmarking can also inform strategic decisions around investor relationships. By having a clear understanding of market-driven pricing trends, lenders can better evaluate their alternatives and optimize their overall execution strategy.

Tracking servicing valuations is another area where benchmarking data proves invaluable. Lenders can analyze loan-level data to determine how their servicing strategies compare with those of their peers. This analysis helps identify opportunities for improving servicing policies and optimizing long-term profitability. In markets where servicing values fluctuate, having a pulse on these changes ensures that lenders remain agile and well-positioned.

Where to Find Actionable Data

Mortgage lenders embracing data analytics are better equipped to navigate the complexities of today’s market and drive profitability.

Optimal Blue's data solutions offer unparalleled access to real-time rate sheet data from over 1,100 originators. This allows users to view the best rate and price offerings tailored to specific scenarios, enabling lenders to make informed decisions throughout the day rather than relying on outdated information. With over 60% of the top 500 lenders using Optimal Blue's pricing engine across retail, correspondent, and wholesale channels, the accuracy of this data is unmatched; it is sourced directly from the Optimal Blue® PPE’s rate sheets rather than surveys.

In addition to rate sheet data, Optimal Blue offers a comprehensive rate lock dataset covering more than one-third of all U.S. residential mortgages, with over 800 lenders actively locking rates. This dataset is the only one of its kind delivered daily and is trusted by the Federal Reserve and other major market participants as a leading indicator of mortgage origination activity. By providing timely insights into rates, volumes, and detailed metrics such as margins and concessions, Optimal Blue empowers users to respond swiftly to market changes, optimizing their pricing strategies effectively.

The extensive data available through Optimal Blue creates significant value across the organization by facilitating deeper analysis of real-time data. This dataset allows for thorough examination of trends across various geographies, enabling lenders to refine their strategies based on detailed insights into rates, price, margins, concessions, LLPAs, servicing values, and production mix by geography. With Optimal Blue, users can optimize their competitive advantages in the dynamic mortgage market, ensuring they are equipped with the most relevant and actionable data to maximize profitability on every loan transaction.

Access more granular pricing insights, the ability to benchmark against the market, post-lock information, competitive analytics, and more through Optimal Blue data solutions.

To learn more, contact Sales@OptimalBlue.com or reach out your Optimal Blue representative.

We Don’t Just Promise ROI. We Power It.

About Optimal Blue

Optimal Blue effectively bridges the primary and secondary mortgage markets to deliver the industry’s only end-to-end capital markets platform. The company helps lenders of all sizes and scopes maximize profitability and operate efficiently so they can help American borrowers achieve the dream of homeownership. Through innovative technology, a network of interconnectivity, rich data insights, and expertise gathered over more than 20 years, Optimal Blue is an experienced partner that, in any market environment, allows lenders to optimize their advantage from pricing accuracy to margin protection, and every step in between. To learn more, visit OptimalBlue.com.

Nothing herein shall be construed as, nor is Optimal Blue providing, any legal, trading, hedging or financial advice.